Understanding Bank Reconciliation: A Step-by-Step Guide

Bank reconciliation is the meticulous art of matching the cash balances on a company's ledger to those in its bank statement, ensuring every penny is accounted for. This process is pivotal for identifying discrepancies such as errors, unauthorized transactions, or timing differences between when a transaction is made and when it is processed by the bank.

Through practical examples, this section will guide readers through the nuts and bolts of the reconciliation process. Imagine a business that issued a check that hasn't yet been cashed, or a deposit made just before the month's end that doesn't show on the bank statement. These scenarios are common, and reconciling helps to highlight and rectify such discrepancies, ensuring the financial statements reflect the true financial position of the business.

As per the Association of Certified Fraud Examiners, businesses lose nearly 5% of annual revenue to fraud and theft. This severely impacts a company’s profitability. Bank reconciliation is crucial for identifying and minimizing such losses.In this article, we will explore the process of bank reconciliation, provide an example of a bank reconciliation statement, offer tips, answer frequently asked questions (FAQs), and demonstrate how to use automation to streamline the reconciliation process.

To broaden your understanding of the reconciliation process and its impact on financial management, explore our detailed guide "What is Account Reconciliation?" at Nanonets. It complements the insights provided in our bank reconciliation discussion.

Learn the significance of utilizing top-tier reconciliation software in the bank reconciliation process at Best Reconciliation Software.

What is Bank Reconciliation?

Bank reconciliation is a critical financial process that involves comparing the transactions and balances on a bank statement with the corresponding records in a company's accounting books. This procedure is essential for identifying discrepancies between the two sets of records, ensuring the accuracy of financial statements, and maintaining the integrity of a company's financial health.

At its core, bank reconciliation aims to verify that every transaction recorded in an organization's cash account matches those listed on the bank statement. This includes deposits, withdrawals, bank fees, and other financial transactions. Discrepancies can arise due to timing differences in recording transactions, errors by the bank or the company, or unauthorized transactions. By reconciling these differences, companies can correct errors, detect potential fraudulent activities early, and accurately report their financial position.

Looking out for a Reconciliation Software?

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

Who is responsible for Bank Reconciliation Activities?

Financial management in companies varies by size and structure. In small companies, few individuals handle multiple financial tasks, while midsize companies introduce specialized roles like accountants or financial managers for day-to-day operations. Larger companies have separate finance, accounting, and treasury departments led by a CFO. The Bank Reconciliation process may be performed by one or more of the following people:

- Business Owner: In many small businesses, especially sole proprietorships or startups, the owner often performs bank reconciliations.

- Bookkeeper: A dedicated bookkeeper is often employed by companies to manage the day-to-day financial transactions of a business, including bank reconciliations.

- Accountant: An accountant may be responsible for bank reconciliations in larger businesses or organizations. Accountants typically have a deeper understanding of financial principles and may perform more complex reconciliations, especially in cases involving multiple accounts or entities.

- Financial Controller: In some companies, especially those with larger finance departments, the financial controller oversees all financial activities, including bank reconciliations. They ensure compliance with accounting standards and internal controls, often delegating reconciliation tasks to staff accountants or assistants.

- Finance Team: In a corporate setting, a team of finance professionals may collaborate on bank reconciliations. This team could include accounts payable and receivable clerks, financial analysts, and other specialists who contribute to the reconciliation process.

- External Auditor: External auditors, hired by the company or appointed by regulatory authorities, may also review bank reconciliations as part of their audit procedures. They ensure that financial statements are accurate and in compliance with accounting standards and regulations.

- Online Bookkeeping Service: For businesses that outsource their bookkeeping functions, an online bookkeeping service may handle bank reconciliations as part of their service package. These services often leverage technology to streamline the reconciliation process and provide real-time financial insights.

How to do Bank Reconciliation?

Typically, businesses receive monthly bank statements either electronically or in paper form, detailing all transactions. The reconciliation process, often conducted monthly, involves meticulously comparing these statements against the business's own financial records. This practice is pivotal for identifying discrepancies, such as timing differences or unauthorized transactions, and rectifying them promptly. By adhering to this routine, businesses maintain the integrity of their financial statements, uphold regulatory compliance, and ensure a true reflection of their financial health.

Step 1: Gather documents

For the bank's part, access to bank statements, uncashed checks, deposits in progress, and any transactions not yet processed is essential. These details can be sourced through paper statements, online banking platforms, or direct integration with your financial management software. Should you manage both a checking and a credit card account, ensure you have statements for each. On the business end, possession of the company's cash book is necessary, documenting all inflows and outflows of cash.

Step 2: Prepare your reconciliation form

When preparing your reconciliation form using this template, you'll start by entering the ending balances provided by your bank and your ledger. The empty rows beneath these entries are intentionally included to allow for adjustments and entries such as outstanding checks, deposits in transit, bank errors, or adjustments necessary to reconcile any discrepancies between the two balances.

| Ending Balance as of 1/31/2020 | ||

|---|---|---|

| Bank Balance | G/L Balance | |

| $11,650 | $10,835 | |

| Ending Balance | ||

As you fill in these details, the "Ending Balance" at the bottom will serve as a summary point, where you will reflect the adjusted balances after accounting for any differences. This systematic approach helps in identifying and rectifying discrepancies efficiently, ensuring that your financial records accurately reflect your true financial position.

The goal is to get your ending bank balance and ending G/L balance to match.

Step 3: Match/Compare deposits

Ensure your bank deposits align with the entries in your general ledger. Banks can err, including transposition mistakes, so it's crucial to verify all deposits are accurately recorded.

Verifying Bank Deposits Tips:

- Accuracy is Key: A misrecorded deposit, say $950 recorded as $95 by the bank, can lead to overdrafts and accruing fees. This step is vital for maintaining your account's integrity.

- Match Deposit Records: Record each cash deposit in the G/L exactly as it was made. For example, if you make three deposits on January 15 of $300, $700, and $150.25, list each separately rather than combining them into a single entry of $1150.25.

- Question Bank Accuracy: While banks are generally reliable, errors can occur. Taking a few minutes to double-check deposit accuracy can prevent potential issues.

Step 4: Compare Checks and Adjust Bank Total

Often, your bank statement may show a higher ending balance compared to your General Ledger (G/L) due to checks and other payments that have not been processed by the bank yet.

To identify these discrepancies, print out your check register for the month and compare it with the cleared checks on the bank's statement. Any issued checks not yet cleared need to be deducted from your bank statement balance.

For example, if you issued checks to two vendors on January 31 totalling $400 and $425, and these have not been reflected by the bank, you'll need to adjust your bank balance accordingly, along with any other outstanding checks.

| Ending Balance as of 1/31/2020 | ||

|---|---|---|

| Bank Balance | G/L Balance | |

| $11,650 | $10,835 | |

| Check #101 | (-$400) | |

| Check #201 | (-$425) | |

| Ending Balance | ||

Step 5: Identify G/L Adjustments

After accounting for outstanding checks, if your bank reconciliation still shows discrepancies, it indicates there are bank adjustments not yet recorded in your General Ledger (G/L). Common adjustments include service fees, overdraft fees, and interest income, which must be recorded in the G/L to finalize the reconciliation.

Tips for Identifying G/L Adjustments:

To pinpoint these adjustments, review your bank statement for any fees and unrecorded deposits. Once identified, adjust your G/L to reflect these items.

Example: Suppose your bank imposed a $25 service fee and credited $10 in interest income. Here's how to reflect these adjustments in a bank reconciliation statement.

| Ending Balance as of 1/31/2020 | ||

|---|---|---|

| Bank Balance | G/L Balance | |

| $11,650 | $10,835 | |

| Check #101 | (-$400) | |

| Check #201 | (-$425) | |

| Service Fees | (-$25) | |

| Interest Income | +$10 | |

| Ending Balance | $10,825 | $10,825 |

Cashbook Balance + Interest - Bank Fees - Rejected Checks = Adjusted Cashbook

Step 6: Compare Balance

After adjustment, the bank balance and cashbook should match. If they are not equal, there is an error in the reconciliation process. Any unwarranted expenses or missing income should be investigated and accounted for during the reconciliation process.

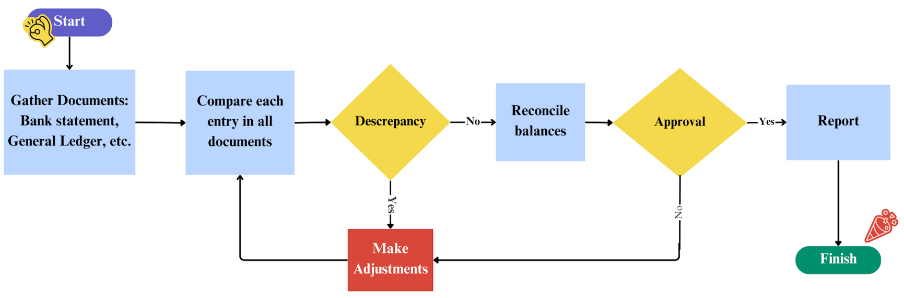

The workflow chart is provided below.

Bank Reconciliation: Important Terms

An understanding of financial terms is essential for anyone performing bank reconciliation as it ensures accuracy and integrity in financial reporting. Some commonly used terms include:

- Bank Statement: A document issued by a financial institution detailing all transactions within a specific period, including deposits, withdrawals, and fees.

- General Ledger: A complete record of all financial transactions of a company, organized by account. It serves as the foundation for preparing financial statements and includes accounts such as cash, accounts receivable, accounts payable, and more.

- Books: The financial records maintained by a company to track its transactions and financial activities. These records, often referred to as the general ledger or accounting ledger, include entries for all financial transactions, such as revenue, expenses, assets, and liabilities.

- Balance per Bank: The ending balance reported by the bank on the bank statement. This figure may differ from the company's records due to outstanding checks, deposits in transit, or bank errors.

- Balance per Books: The ending balance according to the company's internal records such as the General Ledger. It includes all transactions recorded by the company but not yet reflected in the bank statement.

- Reconciliation: The process of comparing the balance per bank with the balance per books and adjusting for any discrepancies to ensure they align.

- Outstanding Checks: Checks issued by the company but not yet presented for payment by the recipient at the bank. These checks reduce the company's balance per books but have not yet been deducted from the bank's balance.

- Deposits in Transit: Funds deposited by the company into its bank account but not yet recorded on the bank statement. These deposits increase the company's balance per books but have not yet been added to the bank's balance.

- Bank Charges and Fees: Service charges or fees levied by the bank for various transactions or account maintenance. These charges may reduce the company's balance per bank.

- Interest Earned: Interest income earned on the company's bank account balances. This amount may increase the company's balance per bank.

- Posting: Transfer of transaction data from various sources, such as journals or subsidiary ledgers, to the general ledger. Posting ensures that all transactions are accurately recorded in the appropriate accounts.

- Bank Reconciliation Statement: A document prepared during the bank reconciliation process that outlines the differences between the company's records and the bank statement. It identifies outstanding checks, deposits in transit, bank errors, and other discrepancies, facilitating the adjustment of the company's records to match the bank's records.

What Is the Purpose of Bank Reconciliation?

The purpose of bank reconciliation is multifaceted, primarily aimed at ensuring the accuracy and consistency of financial records between a company's internal accounts and its bank statements. This process is crucial for identifying discrepancies, such as unrecorded transactions, bank errors, or fraudulent activities, thereby maintaining the integrity of a business's financial statements.

Advantages:

- Error Detection: It helps in spotting errors made either by the bank or within the company’s own accounting processes, such as double entries or transposition errors.

- Fraud Prevention: Regular reconciliation acts as a check against unauthorized transactions, potentially flagging fraudulent activity.

- Cash Flow Management: By accurately knowing the available funds, businesses can make informed decisions about spending, investing, or the need for borrowing.

- Regulatory Compliance: Ensures compliance with accounting standards and regulatory requirements, reducing the risk of penalties or fines for financial inaccuracies.

- Financial Integrity: Maintains the accuracy of financial statements, which is critical for stakeholders, including investors, creditors, and management, to trust in the financial health of the business.

Use Cases:

- A business uses reconciliation to verify that payments made to suppliers have been processed by the bank and to check that customer payments have been correctly deposited.

- Non-profits perform bank reconciliations to ensure donations received are accurately recorded and spent according to their designated purpose.

- Individuals use it to manage personal finances, ensuring their spending and savings align with bank records, preventing overdraft fees and detecting unauthorized transactions.

In essence, bank reconciliation is an essential accounting tool that enhances financial transparency, supports strategic decision-making, and safeguards against errors and fraud.

Types of Bank Reconciliation

Bank reconciliation can be categorized into three primary types, each serving distinct purposes and addressing different aspects of financial management.

1. Internal Reconciliation:

This involves matching transactions within the company's accounting records. For instance, it may include reconciling the cash account in the ledger against receipts or payments records. Internal reconciliation helps ensure that all transactions are accurately recorded and reflected in the company’s financial statements, aiding in the detection of internal errors or discrepancies.

2. External Reconciliation:

External reconciliation focuses on aligning the company's records with external financial statements, typically bank statements. This is the most common form of reconciliation, where the balances of bank statements are compared with the company’s ledger to identify any differences due to outstanding checks, deposits in transit, bank errors, or unauthorized transactions. It's crucial for maintaining the accuracy of cash flow management.

3. Aggregate Reconciliation:

Aggregate reconciliation is used when a company operates multiple accounts and needs to consolidate their balances for a comprehensive overview. This type helps in assessing the overall financial position by combining the individual account reconciliations into a single, aggregated report, providing insights into total cash resources, pending transactions, and potential liquidity issues.

Each type of bank reconciliation serves to enhance financial accuracy, prevent fraud, and support strategic financial planning by providing a clear and accurate picture of financial standing.

How often should you do bank reconciliation?

The frequency of bank reconciliation can vary depending on the size of the business, the volume of transactions, and specific financial management needs. Generally, it is recommended to perform this task at least monthly. This aligns with the typical statement cycle of most banks, allowing businesses to promptly identify and correct discrepancies, manage cash flow accurately, and detect fraudulent activities early.

Different Scenarios:

- Small Businesses or Individuals: For entities with a lower volume of transactions, a monthly reconciliation is often sufficient. This frequency helps maintain a manageable workload while ensuring financial records are accurate and up-to-date.

- Large Businesses: Organizations with a high volume of transactions may benefit from more frequent reconciliations, such as weekly or even daily. This helps in closely monitoring cash flow and promptly addressing any irregularities.

- High-Risk Environments: In sectors or situations with a higher risk of fraud or significant cash transactions, more frequent reconciliations can provide additional security and financial control.

First vs. Second Entries:

The distinction between the first and second entries in bank reconciliation refers to the initial recording of transactions in the company's ledger (first entry) and the subsequent recording or adjustment based on the bank statement (second entry). The first entry is made when a transaction occurs, while the second entry, during reconciliation, corrects or confirms this initial record based on external bank information. This process ensures that internal records are in full agreement with the bank's records, reflecting a true and accurate financial position.

Tips to effectively reconcile bank statements

- Organize your financial records: Maintaining an organized system for storing financial documents is essential. This includes keeping track of receipts, invoices, and bank statements. Consider using digital tools or software to digitize and categorize your documents, making them easily accessible for reconciliation.

- Regular reconciliation: It's crucial to reconcile your bank statements regularly, ideally on a monthly basis. This frequency helps you catch discrepancies early and ensures that errors don't accumulate over time. Regular reconciliation also enhances your ability to manage cash flow effectively.

- Segregate duties: If possible, involve multiple individuals in the reconciliation process. This practice helps reduce the risk of errors and fraud. Separate responsibilities among team members, such as recording transactions, reconciling accounts, and approving discrepancies, to maintain a system of checks and balances.

- Check for timing differences: Be vigilant about timing differences between when transactions are recorded in your financial records and when they appear on the bank statement. Adjust for deposits in transit (deposits you've made but haven't yet cleared) and outstanding checks (checks you've written but haven't been cashed by the payee).

- Review bank statements carefully: Take the time to review each line item on your bank statement thoroughly. Careful scrutiny can help you identify any discrepancies or irregularities that may require further investigation or correction. Pay attention to transaction dates, amounts, and descriptions to ensure accuracy in your records.

- Verify interest and fees: Scrutinize your bank statements for accuracy regarding bank service charges, fees, and interest earned. Ensure that any interest earned is correctly credited to your account, and question any unexpected fees or charges with your bank if necessary. These charges can impact your account balance and financial records.

- Use reconciliation software: Consider leveraging accounting or reconciliation software to streamline the process. Many modern software solutions can automatically sync with your bank accounts, categorize transactions, and provide real-time updates. These tools can significantly reduce manual effort and errors in the reconciliation process.

Benefits of Bank Reconciliation

The benefits of Bank reconciliation extend beyond its immediate operational advantages of promoting financial awareness and transparency to have long-term effects on the overall health of the company. Some long-term benefits include:

- Enhanced Accountability: Accountability fosters a culture of financial responsibility among employees, ensuring that financial resources are used efficiently and transparently.

- Improved Relationship with Stakeholders: Accurate and reconciled financial records instill confidence in stakeholders, including investors, creditors, and regulatory authorities.

- Early Warning System: By identifying discrepancies promptly, businesses can take proactive measures to address underlying issues, such as insufficient funds or irregularities in transaction processing, before they escalate into larger problems.

- Streamlined Audits and Compliance: Well-documented reconciled accounts facilitate smoother audits, reducing the time and resources required for compliance activities and minimizing the risk of penalties or fines for non-compliance.

- Optimized Financial Performance: By providing accurate insights into cash flow and financial transactions, bank reconciliation enables businesses to optimize their financial performance. Identifying areas for improvement, such as reducing unnecessary expenses or optimizing revenue streams, helps businesses achieve greater efficiency and profitability.

- Facilitated Decision-Making: Timely and accurate financial information resulting from bank reconciliation facilitates data-driven decision-making. Managers can rely on reconciled financial data to evaluate performance, assess the impact of strategic initiatives, and make informed decisions that drive the company's growth and success.

Prevention of Financial Losses: By promptly identifying and resolving issues, businesses can safeguard their assets and minimize the risk of financial loss, protecting the long-term viability of the organization.

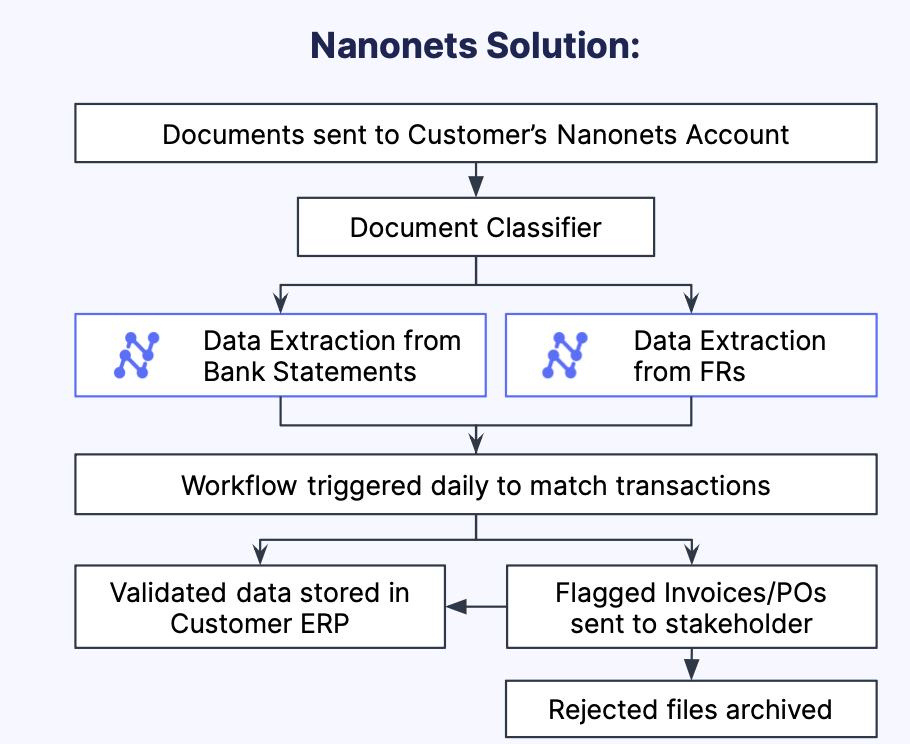

Automate Bank Reconciliation on Nanonets

Bank reconciliation is a time-consuming process with many manual steps. Most automation tools provide OCR capability that extracts relevant information from documents. However, this is just one aspect of your workflow. You need a tool to build a customized workflow, automating business logic while integrating with existing tools.

Nanonets is an AI-powered workflow automation solution that simplifies and streamlines account reconciliation. It automates various steps, reduces manual effort, and increases efficiency by 10x.

Automate your mortgage processing, underwriting, fraud detection, bank reconciliations or accounting processes with a ready-to-use custom workflow.

The Nanonets bank reconciliation workflow works like this:

- Automated import: Nanonets can automatically import documents like bank statements from mail or through the bank API.

- Data extraction: Nanonets uses state-of-the-art optical character recognition (OCR) technology to extract relevant data accurately. This eliminates the need for manual data entry, which can save time and reduce errors.

- Data matching: Nanonets allows you to set up a rule-based matching to identify and reconcile transactions across different systems. This helps ensure that all transactions are accounted for and there are no errors.

- Approval: Nanonets can automate the account reconciliation process, from data entry to approval. This can free up time for accountants to focus on other tasks.

- Centralized repository: Nanonets provides a central repository for supporting documentation. This makes it easy to find and access documents when needed.

If Nanonets meets your business requirements, you can get in touch for a customized quote.

An Example of Bank Reconciliation

ABC Enterprises, a small retail company, conducts bank reconciliation for June. ABC processes customer payments, pays suppliers, and incurs various operating expenses. During the month-end reconciliation process, ABC Enterprises identifies discrepancies between its internal records and the bank statement:

- Two checks totaling $1,500 issued to suppliers have not yet cleared the bank.

- A customer payment of $2,000 made via electronic transfer on June 30th is not reflected in the bank statement.

- The bank has charged a monthly service fee of $30, which ABC Enterprises was not previously aware of.

To reconcile its accounts, ABC Enterprises takes the following steps:

- ABC updates its internal records to reflect the outstanding checks and deposits in transit, ensuring alignment with the bank statement.

- ABC contacts the bank to inquire about the unprocessed deposits and clarify any unexpected fees. They request documentation to support the charges and negotiate where applicable.

- ABC implements controls to prevent future discrepancies, such as regularly monitoring outstanding checks and deposits, reviewing bank statements promptly, and negotiating favorable banking terms to minimize fees.

To overcome challenges associated with bank reconciliation, ABC Enterprises leverages technology solutions such as Nanonets for automation. They also invest in employee training to ensure proficiency in reconciliation procedures and compliance with regulatory requirements.

Take Away

From small businesses to large corporations, maintaining precise financial records and reconciling them with bank statements is essential for informed decision-making, regulatory compliance, and stakeholder confidence. By understanding the importance of bank reconciliation and implementing effective reconciliation procedures, companies can navigate financial challenges, mitigate risks, and position themselves for long-term success. As technology continues to advance and regulatory requirements evolve, ongoing attention to bank reconciliation remains crucial for financial health and operational efficiency in the ever-changing business landscape.

FAQs

What are the 4 steps in the bank reconciliation?

Compare records: Match your internal financial records with the transactions listed on the bank statement to identify any discrepancies.

Adjust balances: Factor in any outstanding checks, deposits in transit, bank fees, and errors to adjust the balance of your financial records accordingly.

Journalize differences: Make the necessary journal entries for discrepancies between your records and the bank statement after adjustment.

Verify final totals: Review the adjusted book balance and the adjusted bank balance to ensure they are now reconciled and the same.

If there are differences, investigate and resolve them to ensure that the records are accurate, complete, and within the financial reporting framework.

How do you reconcile a bank statement?

To reconcile a bank statement, compare your internal ledger against the bank statement for the same period. Identify any mismatched transactions, such as deposits in transit and outstanding checks. Adjust for bank errors, fees, and interest. Make journal entries for these adjustments and review the final reconciled balance to confirm that the records align.

What is BRS in simple words?

Bank Reconciliation Statement (BRS) is a document that matches the cash balance on a company's balance sheet to the corresponding amount on its bank statement, reconciling any differences to ensure that the figures are accurate and consistent. It serves as a check to verify that all transactions have been recorded correctly in the company's and the bank's records.

Is bank reconciliation debit or credit?

Bank reconciliation itself is neither a debit nor a credit. It is a process of comparing the balances and transactions in one's accounting records against the bank statement to identify any discrepancies and make the necessary adjustments to the accounting records.

What are the steps to reconcile a bank statement?

Identify discrepancies:

Compare each transaction from your accounting records with those listed on the bank statement to spot any differences.

Add or subtract adjustments:

Record any bank fees, interest income, or errors found on the bank statement that are not yet in your accounting records.

Record outstanding items: Account for any outstanding checks or deposits that have not cleared the bank.

Reconcile and verify: After accounting for all differences, ensure the adjusted bank statement balance matches your reconciled internal records.

How do I reconcile a bank statement in Excel?

Use Nanonets to extract transaction data from your bank statement, then export it to Excel. Create a reconciliation template and annotate each column for deposits, withdrawals, bank fees, and checks. Import your ledger data and use Excel’s sorting and filtering tools to match transactions. Apply formulas to calculate differences automatically and use pivot tables to summarize the data. Adjust for any outstanding items and verify that the ending balances match to complete the reconciliation process.